Homeseeking is a rush of exhilaration and uncertainty. You search high and low for a home. Anticipation. You find one. Excitement. You make an offer. Anxiety. You wait for the response. Dread, hope, dread, hope. You enter a bidding war. Terror. Pep talk. Hope again. Dread. Fear. Hope. Mild insanity. And then… it gets accepted. Whooohoooooooooo. And exhale.

Now to apply to a lender and get mortgage approved. But you were a good student and got pre-approved through a mortgage broker before starting out on homeseeking journey. They negotiated on your behalf with a few different lenders and a lender offered you a mortgage in principle at a favourable interest rate. We locked in that rate for 120 days for you and the clock hasn’t run out yet. You high five yourself because in the interim interest rates have gone up and you are safe for 5 years from the effects of the increase.

The lender does a thorough background check as well as a home inspection and you are officially approved and you close the deal. Well done, you well-prepared and diligent homeseeker.

This sounds like the ideal scenario, especially if you are risk averse. With the ups and downs of the homeseeking process, having a rate hold can provide a measure of certainty. So it must be worth the focus placed on it by everyone who ever talks real estate, right? Well, let’s see.

Some explanations of what this whole rate hold business means:

Pre-approval: A process used by mortgage lenders to identify how much money they will lend to you after doing a detailed assessment of your financial situation. It is not a guarantee for a mortgage from a lender. Rather, it indicates what you can afford to borrow and what mortgage rate you qualify for in principle.

Interest rate: The rate a lender adds to a mortgage as the cost for borrowing the sum of money. Usually expressed as a percentage on top of the principal amount you borrow and have to pay back over time.

Rate hold: The amount of time, usually between 60 and 120 days, that a lender will guarantee a loan's interest rate after giving you pre-approval, and before offering you a firm commitment of a mortgage.

Fixed rate: With a fixed-rate mortgage loan, the interest rate secured with the lender remains the same through the term of the loan.

Variable rate: A variable-rate on a mortgage loan is calculated according to the prime rate and will move up and down with the prime, which is primarily influenced by the policy interest rate set by the Bank of Canada (BoC), also known as the overnight rate.

Float down: If you have a fixed-rate mortgage, a float-down option allows you to reduce your mortgage interest rate if prime rates dip below your rate hold.

So what should you do?

In the business of getting mortgage approval, the big question is always whether to go with fixed or variable rate. Pre-Covid, a fixed-rate was the going option. Then boom, the world turned upside down and suddenly a variable-rate option made the most sense. But now, interest rate hikes have changed the game again and once more a fixed rate might be the best choice. Well, until the next unforeseen world event shakes us all up again.

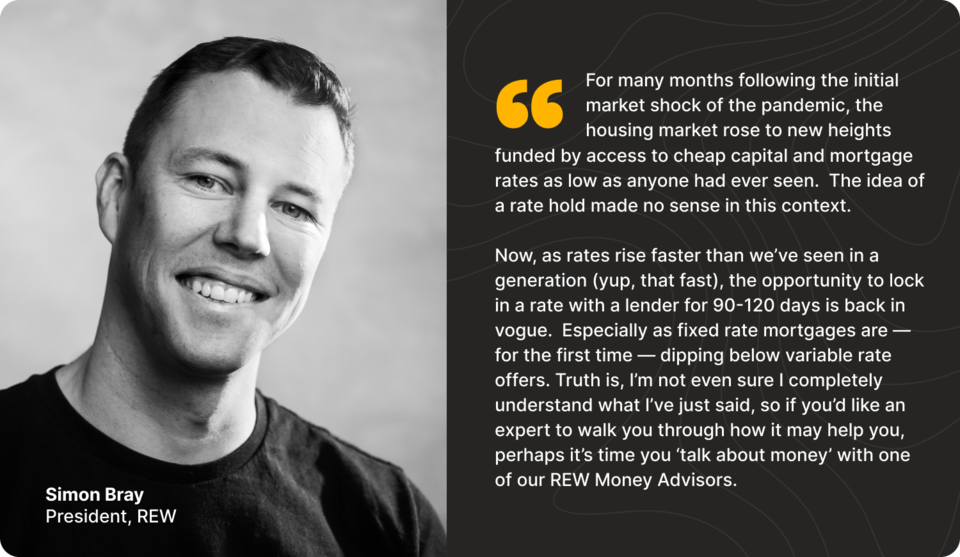

Everyone has a different opinion, including Cole Hennig, REW sales director. But what does REW president Simon Bray think?